Let me be honest with you. Finding the right best AI budgeting apps for beginners in USA feels overwhelming. You open the App Store, see dozens of options, and most of them promise to fix your money problems overnight. Some look incredibly simple until you actually start using them. Others have so many features you need a finance degree just to understand the dashboard.

I get it. You probably got here because you’re tired of wondering where your money disappears every month. Maybe you know you should be saving more, but manually tracking expenses on a spreadsheet sounds like torture. Or perhaps you’re stuck in the paycheck to paycheck cycle and have no idea how to break free.

This is where best AI budgeting apps for beginners in USA come in.

These apps are designed differently than traditional money management tools. They learn from your spending patterns. They automatically categorize your transactions instead of making you manually tag every coffee purchase. They alert you when something unusual happens. Most importantly, they work in the background while you sleep, getting smarter about your finances without requiring hours of setup or complex understanding.

The Federal Reserve’s recent survey shows something important: most Americans don’t have financial visibility. Nearly 37 percent of U.S. adults say they cannot cover a 400 dollar emergency expense with cash. This isn’t a question of income. It’s a question of awareness. Many people earn decent money but have no system to track where it actually goes.

That’s the problem best AI budgeting apps for beginners in USA solve.

Here’s what this guide covers. I’ve tested seven different best AI budgeting apps for beginners in USA specifically designed for someone just starting their money management journey. I’ve set them up from scratch, used them for weeks, and reviewed how each one actually performs. This isn’t theoretical advice. These are real apps that real people use successfully.

But before you download anything, understand this one thing: no app fixes money problems by itself. An app shows you the truth about your spending. It removes the manual work. It creates reminders and alerts. But you still need to make the actual decisions. You still need to be willing to look at your finances honestly.

This article is educational information only and should not be considered financial advice. Always consult a qualified financial professional before making major financial decisions.

Understanding What Makes a Budgeting App Work for Beginners

Before diving into specific apps, let’s talk about what actually matters when you’re just starting out.

The biggest mistake beginners make is choosing based on features instead of simplicity. An app with fifty features doesn’t help you if it takes thirty minutes to understand the dashboard. You need something that answers your questions in seconds, not an app that requires you to read a manual.

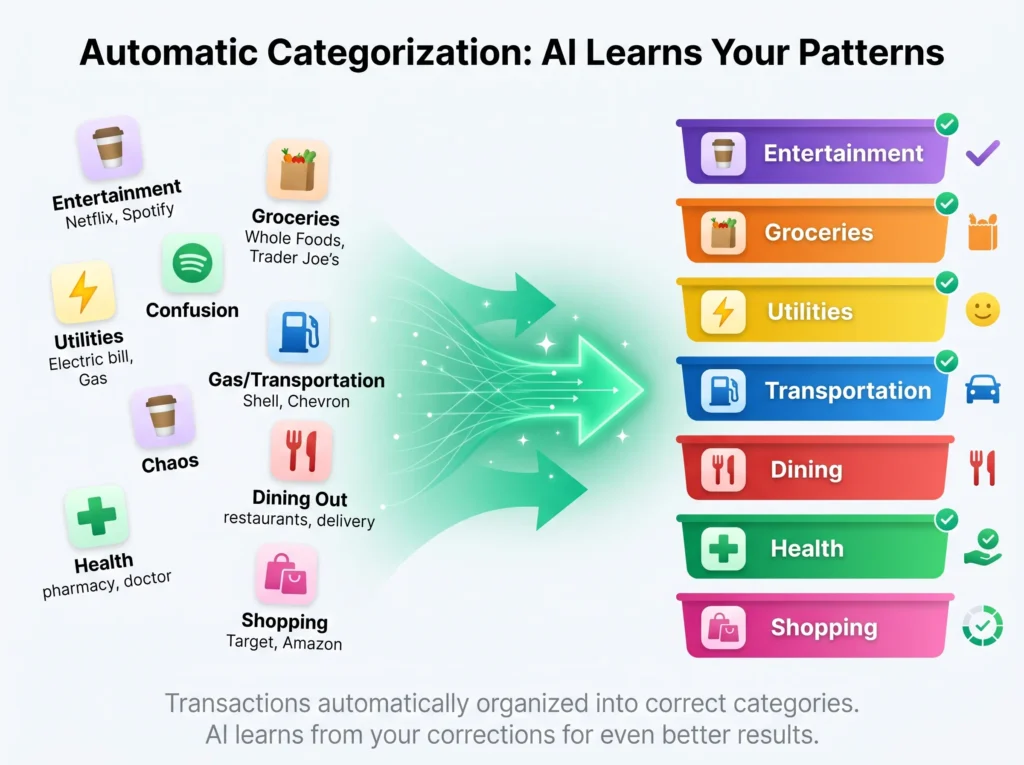

Automatic Categorization

Automatic categorization is where everything starts. When you connect your bank account, the app should instantly organize your transactions. Netflix goes under Entertainment. Whole Foods goes under Groceries. Your electric bill goes under Utilities. More importantly, the app learns from your patterns. If you always go to the same coffee shop and it gets miscategorized once, you correct it, and the app remembers for next time. This is where AI actually makes a difference.

Clear and Simple Answers

The second thing you need is a clear answer to a simple question. For most beginners, this question is: Do I have money to spend right now? Some apps show this through a dashboard. Some explain it through a chat interface. Some visualize it with progress bars. The method doesn’t matter as much as getting a clear answer quickly.

Mobile Access and Speed

Mobile access matters more than most people think. You need to check your budget while you’re standing in a store deciding whether to buy something. This means the app needs to be fast, responsive, and actually useful on a phone. Not just “available on mobile” but genuinely designed for the mobile experience first.

Security Standards

Security is non-negotiable. When you connect a budgeting app to your bank account, it uses secure financial data connections. The app gets read-only access, which means it can see your transactions but cannot move money or access your passwords. This is industry standard, but it’s worth understanding before connecting accounts.

A Quick Look at Your Budgeting App Options

Before diving into detailed reviews, here’s a snapshot of the seven best AI budgeting apps for beginners in USA that I tested. This gives you a quick way to see which might match what you’re looking for.

Cleo works through conversation. You chat with an AI assistant about your finances, and it explains spending patterns in human language. Best for people who want guidance and feel intimidated by traditional dashboards.

Copilot Money focuses on visual design. Everything is clean, modern, and beautiful. It brings together spending, investments, and net worth on one screen. Best for people who want a premium experience and are willing to pay for it.

PocketGuard emphasizes one number: how much you can safely spend today. It tracks your money through three categories: committed spending, goal spending, and discretionary spending. Best for people who want the simplest possible answer.

Monarch Money goes in the opposite direction. It shows everything about your financial life in one place. All accounts, all investments, household spending, net worth growth. Best for people who want to see the complete picture.

Rocket Money specializes in catching subscriptions and recurring charges you forgot about. It automatically finds them and can help you cancel them with one tap. Best for people whose biggest problem is subscription overload.

YNAB teaches a specific budgeting philosophy. It’s more structured and requires more effort, but it creates behavior change. Best for people who want to learn a system, not just track spending.

Chime is technically a banking app, but it includes spending tools and automatic savings features. It’s useful if you want banking and budgeting in one place. Best for people who want simplicity and aren’t loyal to any particular bank.

Detailed Review of Each Best AI Budgeting App for Beginners

Cleo: Easiest for Conversation Based Learning

Cleo works fundamentally differently from other budgeting apps. Instead of logging in to a dashboard, you open the app and chat with an AI assistant about your finances. You ask questions in plain English, and Cleo responds with insights and advice.

This approach removes the intimidation factor for absolute beginners. You don’t need to understand what a “zero-based budget” is or interpret complex charts. You just talk about your money like you’d talk to a friend who happens to know a lot about finance.

What you actually get with Cleo is spending insights that appear as you chat. The app categorizes your transactions automatically and shares patterns with you conversationally. It helps you set savings goals. It alerts you to recurring subscriptions. It offers cash advance features if you need emergency cash before payday. Most importantly, it explains everything in a friendly tone instead of jargon.

Why Cleo Works for Beginners

For beginners, Cleo’s biggest advantage is reducing stress. Money conversations feel less scary when they’re just messages in your phone. You can ask a question anytime, even at two in the morning when you’re worried about bills.

Pricing and Cost

Pricing ranges from free access with basic features to paid subscriptions starting at 5.99 per month for additional features. The free version is genuinely useful, so you can test whether the app works for you before paying anything.

Main Limitations

The main limitation is that Cleo isn’t ideal if you want traditional budgeting control. If you’re the type who likes detailed spreadsheets and wants to assign every dollar to a specific purpose, this app will feel too casual. But if you want encouragement and guidance, Cleo delivers.

Final Verdict on Cleo

Cleo is a strong first choice for beginners who want a simple, guided, conversational money app.

Copilot Money: Best for a Premium Experience

Copilot Money is for people who appreciate good design. Everything about this app looks like it was designed by people who actually care about the experience. The interface is clean. The colors work well together. Information appears where you need it without unnecessary clutter.

The app connects your checking account, savings account, credit cards, loans, and investments. It shows you spending broken down by category. It displays upcoming bills so you never miss a payment. It calculates your net worth and shows you how it changes over time. For people who want one place to see everything financial, this is compelling.

What Makes Copilot Different

What makes Copilot different from other all-in-one apps is the attention to visual design. Many finance apps feel clinical. This one feels like it was designed by designers, not just engineers. That matters more than you’d think. When your budgeting app is a pleasure to use, you actually open it instead of avoiding it.

Copilot also includes subscription tracking and bill negotiation features. It finds recurring charges and suggests which ones you might want to cancel. The net worth tracking is particularly useful for beginners who want to see progress over months and years.

Pricing Structure

Pricing sits around 13 dollars per month or 95 dollars per year, making it more expensive than casual budgeting apps but less expensive than hiring a financial advisor. A free trial lets you test it before committing.

Trade-offs to Consider

The tradeoff is complexity. Copilot is more powerful than Cleo, which means it’s less beginner friendly if you only want one simple number. But if you like seeing your full financial picture and have the time to explore the features, this app grows with you as you become more financially sophisticated.

Copilot Money Verdict

Copilot Money is one of the best choices for beginners who want a premium, polished, all-in-one money dashboard.

PocketGuard: Simplicity as the Ultimate Feature

PocketGuard answers one question: How much can I safely spend right now?

That’s it. That’s what the app does.

You connect your checking account, and PocketGuard shows you three categories. There’s money committed to bills you’ve already promised to pay. There’s money for goals you’ve set, like saving for vacation or an emergency fund. And there’s money you can actually spend on whatever you want without derailing your finances.

Why PocketGuard Matters for Beginners

For beginners, this is powerful simplicity. You’re not staring at complex dashboards trying to understand whether your spending is good or bad. You’re getting one clear answer every time you open the app. And that answer changes in real time as you spend money and as bills get paid.

PocketGuard also tracks subscriptions, reminds you about upcoming bills, and helps you stick to budgets for specific categories if you want that level of detail. But the core feature is that safe to spend number.

Cost and Affordability

Pricing is approximately 6.25 dollars per month with annual billing. It’s one of the cheapest options, and the free version is useful enough that many people never upgrade.

Limitations to Know

The limitation is exactly what makes it simple. If you want detailed reports, investment tracking, or household financial planning, you won’t find it here. But if you want to stop overspending and regain financial control, PocketGuard excels at solving that specific problem.

PocketGuard Final Assessment

PocketGuard is a great option for beginners who want simple spending control without learning a complex budgeting system.

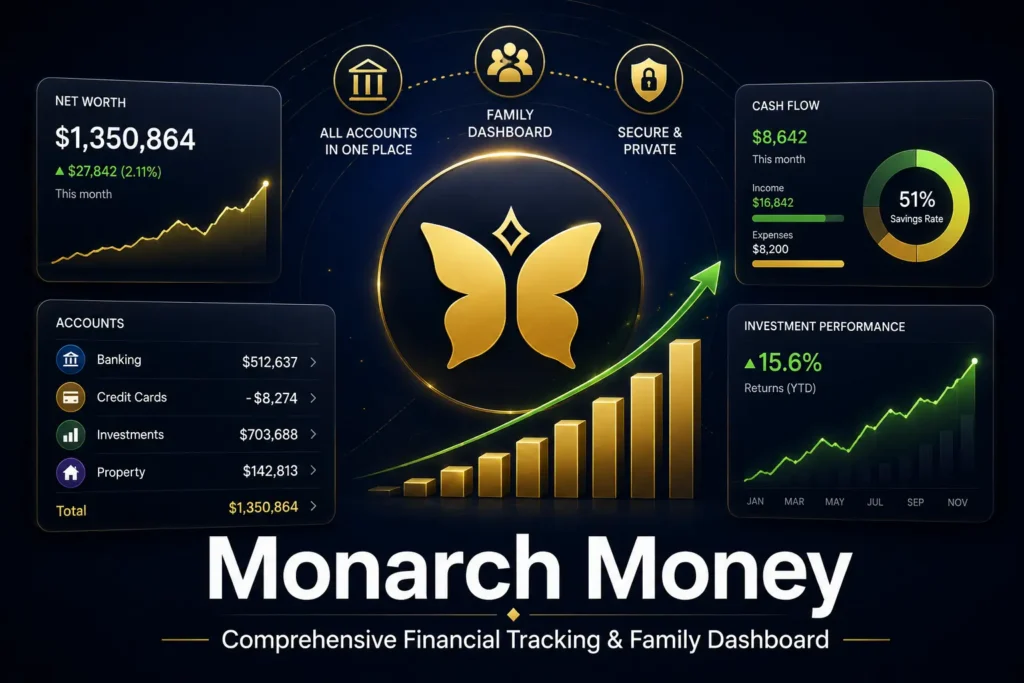

Monarch Money: Your Complete Financial Dashboard

Monarch Money takes the opposite approach to PocketGuard. Instead of simplifying down to one number, it shows you everything.

You can connect bank accounts, credit cards, loans, mortgages, brokerage accounts, cryptocurrency wallets, real estate, and more. The app calculates your complete net worth. It shows spending by category. It identifies recurring subscriptions. It shares reports and insights. For people who want to understand their entire financial picture, this is the app.

Monarch for Couples

Monarch is particularly useful for couples managing finances together. Both people can see the same dashboard, so there’s transparency about household spending. You’re not guessing who paid what or whether you’re within budget.

Learning Curve Reality

The learning curve is higher than Cleo or PocketGuard. But once you understand the interface, it becomes powerful. The reports show spending trends. The net worth tracking shows progress. The subscription detection finds money you’re wasting.

Pricing Details

Pricing runs around 14.99 per month or 99 dollars per year, with a free trial so you can test it first. This price point puts it in the premium category, but if you’re managing money with a partner or want comprehensive financial visibility, it’s a worthwhile investment.

Monarch Money Recommendation

The main consideration is that Monarch requires more time to set up and understand than beginner apps. But if you’re willing to spend an hour learning the interface, you get powerful visibility into your complete financial situation.

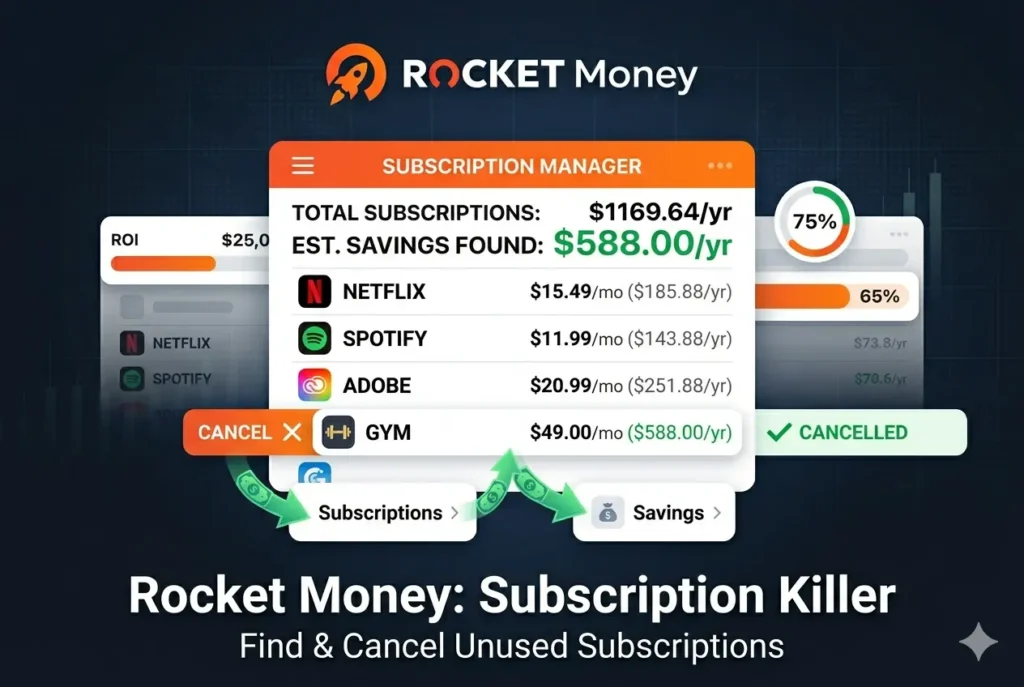

Rocket Money: The Subscription Problem Solver

Rocket Money exists to solve one specific problem: you’re paying for stuff you forgot about.

Most Americans lose track of subscriptions. That streaming service you tried once and never cancelled. The gym membership you signed up for in January and never used. The software subscription that sounded useful but turned out not to work for you. These accumulate to hundreds of dollars per year for many people.

Rocket Money automatically finds all your subscriptions and recurring charges. It shows you a list with the amount you pay and how often. More importantly, it can help you cancel unwanted subscriptions with one tap. For some services, you can even cancel directly in the app.

Beyond Subscriptions

Beyond subscriptions, Rocket Money includes basic budgeting, bill reminders, spending tracking, and custom categories. But the core value is in subscription management.

Pricing and Value

Pricing includes a free version that handles subscription tracking, and premium plans from 7 to 14 dollars per month for additional features. Many people find the free version sufficient.

Immediate Return on Investment

For beginners whose biggest financial problem is subscription waste, this app pays for itself immediately. Finding even five unwanted subscriptions at 10 dollars per month each saves you 600 dollars per year. That’s more than enough to justify using the app.

What Rocket Money Doesn’t Do

The limitation is that Rocket Money isn’t a complete budgeting system. You can do basic budgeting, but if you want detailed financial planning or investment tracking, you need something else.

Rocket Money Final Thoughts

Rocket Money is a smart choice if your first goal is to reduce waste and cancel subscriptions you no longer use.

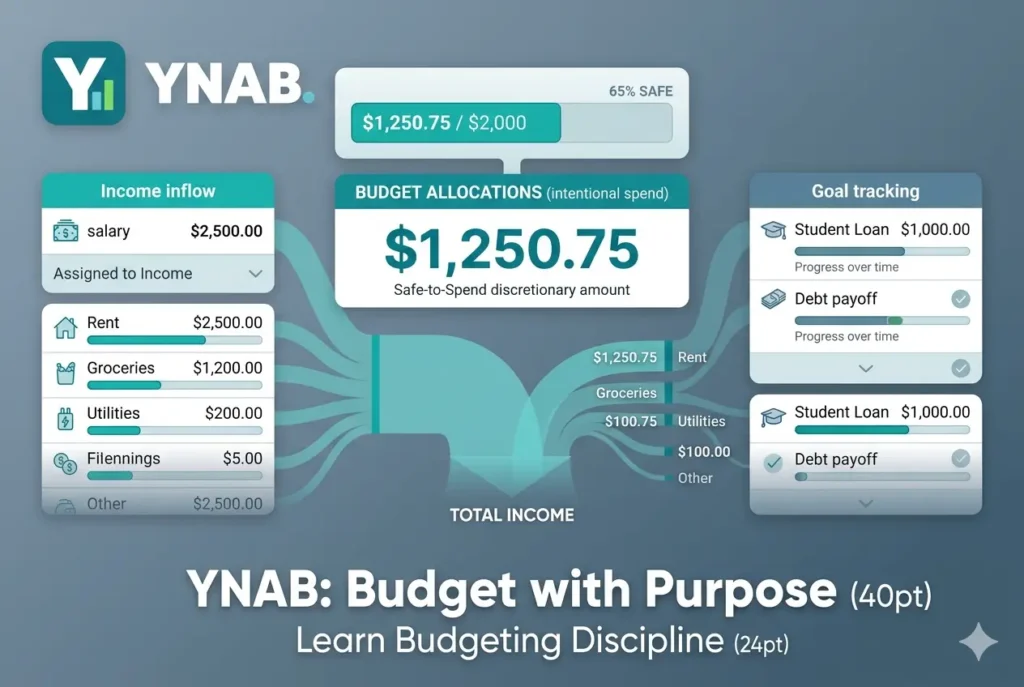

YNAB: Learning Real Budgeting Discipline

YNAB stands for You Need A Budget, and it’s fundamentally different from the other apps on this list.

YNAB teaches a specific budgeting philosophy called zero-based budgeting. The idea is simple but powerful: every dollar you earn gets assigned to a specific purpose before you spend it. You don’t make a budget and hope you stick to it. You actively decide where each dollar goes.

This approach creates behavior change because you’re making conscious decisions instead of just reacting to your spending. You decide that this paycheck includes 200 dollars for groceries, 80 dollars for gas, 50 dollars for entertainment, and the rest toward savings goals. When you spend money, you watch those allocations change in real time.

YNAB Features and Tools

YNAB also includes goal tracking, spending reports, and the ability to manually enter transactions if you prefer that to automatic syncing. It works on every device, so you have consistent budgeting whether you’re on your phone or computer.

Cost and Commitment

The commitment is significant. YNAB costs 14.99 per month or 109 dollars per year. There’s a 34-day free trial, but there’s no free version after that.

More importantly, YNAB requires more effort than other apps. You’re not just passively reviewing data. You’re actively managing your budget. You’re thinking about every dollar. This is powerful for people who want to change their financial behavior, but it’s a lot for someone who just wants to see where their money goes.

Who Should Choose YNAB

For beginners specifically, YNAB is best if you’re serious about change and willing to invest time and money in learning a budgeting system. It’s not the right choice if you want something quick and easy.

YNAB Verdict

YNAB is best for beginners who want structure, discipline, and long-term behavior change.

Chime: Banking Meets Savings Automation

Chime is a mobile banking app, not an AI budgeting app. But it deserves inclusion because it combines banking with useful financial features.

When you open a Chime account, you get a checking account, debit card, and mobile app for managing money. You can set up direct deposit, pay bills, transfer money, and see your balance anytime.

What Makes Chime Interesting

What makes Chime interesting for budgeting is its savings automation features. You can set up automatic transfers to savings on payday. You can use round-up features that take your spare change and move it to savings. You get an early direct deposit, so you see your paycheck two days early. These features help beginners build saving habits without requiring discipline.

Chime also includes spending visibility, so you can see where your money goes. It’s not as detailed as dedicated budgeting apps, but it’s useful for basic awareness.

Pricing Model

Pricing is simple: no monthly fee for the core banking services. Chime makes money through transaction fees and third-party services, not by charging you to use the app.

Important Consideration

The trade-off is that using Chime means switching to their banking service. If you’re deeply committed to your current bank, that’s a deal-breaker. But if you’re open to trying a new bank and you want automatic savings features, Chime offers genuine value.

Chime Final Assessment

Chime is best as a banking-plus-savings option, not as a complete replacement for a budgeting app.

How to Choose the Right App for Your Situation

The worst decision is overthinking this choice. Each of these apps solves different problems, and the “best” best AI budgeting app for beginners in USA is the one that matches what you actually need.

If you’re a complete beginner and feel intimidated by financial apps, start with Cleo. The conversational interface removes the feeling that you need to understand complicated finance concepts. Just talk to your app like it’s a friend.

If your main struggle is overspending between paychecks, PocketGuard solves that specific problem. Knowing exactly how much you can safely spend is powerful.

If subscriptions are your biggest financial leak, Rocket Money immediately pays for itself by finding subscriptions you forgot about. Get quick wins by cancelling unused services.

If you want a premium experience with beautiful design and comprehensive features, Copilot Money is worth the monthly fee. It feels good to use, which matters more than you’d think.

If you manage money with a partner and want complete financial transparency, Monarch Money’s shared dashboard is valuable. You can see household finances together.

If you’re serious about changing your relationship with money and willing to learn a budgeting system, YNAB creates behavior change through intentional money allocation.

If you’re open to switching banking services and want automatic savings, Chime combines banking with savings automation.

Realistically, most beginners should start with one of the first three options: Cleo, PocketGuard, or Rocket Money. These are approachable, affordable, and solve real beginner problems without overwhelming you.

Comparison Table of Best AI Budgeting Apps for Beginners

| App Name | Best For | Ease of Use | Free Option | Starting Price | Rating |

|---|---|---|---|---|---|

| Cleo | Chat-based learning | Very easy | Yes | $5.99/month | 9.8/10 |

| Copilot Money | Premium dashboard | Easy | Trial | $13/month | 9.6/10 |

| PocketGuard | Simple spending control | Very easy | Yes | $6.25/month | 9.4/10 |

| Monarch Money | Full financial view | Moderate | Free trial | $14.99/month | 9.3/10 |

| Rocket Money | Subscription tracking | Easy | Yes | $7-14/month | 9.1/10 |

| YNAB | Budgeting discipline | Moderate | 34-day trial | $14.99/month | 8.9/10 |

| Chime | Banking and savings | Easy | Yes | Free | 8.7/10 |

Setting Up Your First Best AI Budgeting App

Once you’ve chosen an app, the actual setup is simpler than you’d expect.

Start by downloading the app to your phone. Create an account using your email address and a strong password. Most budgeting apps ask for two-factor authentication, which adds security. Turn this on.

Connecting Your Bank Account

Next, you’ll see an option to connect your bank account. This is the moment most beginners hesitate, worried about security. The reality is that reputable budgeting apps use the same secure connections that banks use. The app gets read-only access, meaning it can see your transactions but cannot move money or access your account. This is industry standard and safe.

Start with your main checking account only. Don’t connect everything on day one. Let the app pull in your last 30 days of transactions. Review the categories. Most apps automatically categorize transactions, but the first time through, you’ll probably see mistakes. Correct them. Each correction helps the app learn.

Setting Your First Goal

Now spend a few minutes setting one goal. Not five goals. One. Maybe it’s saving 500 dollars in the next three months. Maybe it’s reducing dining out spending by half. Maybe it’s finding and cancelling unused subscriptions. Pick one goal that would genuinely improve your financial situation.

Turn on notifications. Most apps let you set alerts for unusual spending, upcoming bills, low balance warnings, or subscription renewals. These alerts keep budgeting top of mind without being annoying.

Building the Habit

Then just use the app for a week. Open it daily for a few minutes. Look at the dashboard. See what’s happening with your money. This daily habit is what transforms budgeting from something you plan to do into something that actually happens.

Common Mistakes Beginners Make With Best AI Budgeting Apps

After someone starts using a budgeting app, certain patterns emerge. Let me share the mistakes I see most often.

Too Many Apps at Once

The first mistake is downloading too many apps at once. You think maybe you need Cleo and Rocket Money and Copilot all running simultaneously. What actually happens is confusion. You’re checking multiple dashboards. You’re comparing numbers that don’t match. You’re getting overwhelmed. Resist this urge. Start with one app. Master it for 30 days. Only then consider adding a second app if you genuinely need it.

Not Reading Pricing Details

The second mistake is not reading the pricing details before connecting your card. Many apps have free versions, paid upgrades, and free trials. If you connect a payment method without understanding what you’re signing up for, you might get surprised by a charge you weren’t expecting. Spend five minutes reading the pricing page before entering any payment information.

Expecting Instant Results

The third mistake is expecting instant results. You set up the app on Monday and expect to be saving thousands by Friday. It doesn’t work that way. The app shows you patterns quickly, but behavior change takes time. Real habit formation takes 30 to 60 days. Commit to at least 30 days of daily app usage before deciding whether it’s working.

Connecting Too Many Accounts

The fourth mistake is connecting every account on day one. You link your checking account, savings account, credit cards, and investments all at once. Now you’re overwhelmed by data. Start small. Just the main checking account. After a week, add your credit card if you want. After another week, add savings. Build the habit gradually.

Ignoring Security Practices

The fifth mistake is ignoring security practices. Don’t connect financial apps to accounts with weak passwords. Don’t use the same password across multiple services. Don’t ignore the app’s security recommendations. These apps hold sensitive information. Treat them accordingly.

Treating AI as Professional Advice

The sixth mistake is treating the app as financial advice. AI can organize your data and show you patterns, but it can’t replace professional advice for taxes, major debt decisions, or investment strategies. Use the app for organization and awareness. Consult professionals for major financial decisions.

Real Examples of How Beginners Use Best AI Budgeting Apps

Let me share some realistic scenarios to show how these apps actually help.

Sarah’s Subscription Discovery

Sarah is working full-time but feels like money disappears every month. She has no idea where it goes. She downloads Rocket Money and discovers she’s paying for five streaming services she barely uses, a gym membership she hasn’t visited in a year, and two cloud storage subscriptions she forgot existed. That’s 180 dollars per month she didn’t realize she was spending. She cancels the unused services and redirects that money to an emergency fund. In three months, she’s saved 540 dollars.

James’ Paycheck Management

James is paycheck-to-paycheck and nervous about money. He starts Cleo because the chat interface feels less stressful than traditional apps. Just talking to the app about his spending makes him feel less anxious. Over a month, Cleo helps him understand his patterns and identifies areas where he’s overspending. By the second month, he’s managing his paycheck better and actually has money left over at the end of the month.

Marcus and Jennifer’s Joint Finances

Marcus and Jennifer are married and handle money separately. They start Monarch Money to see their combined finances together. For the first time, they both understand the complete household picture. They notice duplicate spending on some subscriptions because they were each buying without knowing the other already had it. Seeing their finances together increases communication and alignment about money goals.

Alex’s Debt Payoff

Alex is dealing with credit card debt and wants to change habits. They commit to YNAB even though it requires more effort than other apps. The process of assigning every dollar to a purpose before spending it forces conscious decisions. Instead of just paying the minimum and hoping debt goes away, Alex creates an aggressive payoff plan. The app motivates the behavior change needed to actually make progress on debt.

These aren’t fantasy scenarios. These are realistic situations that happen when someone finds an app that matches their needs and uses it consistently.

Frequently Asked Questions About Best AI Budgeting Apps for Beginners

What is the best AI budgeting app for beginners?

It depends on what you specifically need. Cleo is easiest for conversation-based learning. PocketGuard is best if you want one simple answer about spending. Rocket Money is best if subscriptions are your problem. If you want premium design and features, Copilot Money is worth the cost. There’s no single best app for all beginners. There’s a best app for your specific situation.

Are AI budgeting apps secure?

Reputable apps use bank-level encryption and secure financial data connections. The app gets read-only access to your account, meaning it can see transactions but can’t move money. This is industry standard. That said, you should still check each app’s privacy policy and security certifications before connecting accounts. Avoid unknown apps with unclear privacy practices.

Will a budgeting app actually save me money?

A budgeting app doesn’t directly save you money. What it does is create visibility and remove manual work. When you see clearly where your money goes, you make better decisions. When the app reminds you about subscriptions or alerts you to unusual spending, you take action. When you set a goal and track progress, you’re more motivated. But the app is a tool. Your actions create the results.

Which app is best for managing money with a partner?

Monarch Money is specifically designed for shared finances and household visibility. Both people can see the complete financial picture. This transparency supports better communication about money.

Should I pay for a premium budgeting app or stick with free versions?

Most beginners should start with free versions. Test the app. See if it actually helps. Only pay if the premium features address a real need. Many people find free versions completely sufficient.

How long should I use an app before deciding if it’s working?

Give yourself at least 30 days. That’s long enough to connect accounts, understand the interface, correct categorization mistakes, set goals, and build a habit. Snap judgments after three days don’t tell you whether an app actually works.

Can an AI budgeting app replace a financial advisor?

No. Budgeting apps are tools for tracking and organization. Financial advisors provide personalized guidance based on your complete situation, goals, and challenges. For budgeting and spending awareness, an app is sufficient. For financial planning, tax strategy, or investment decisions, consult a professional.

Final Thoughts on Getting Started With Best AI Budgeting Apps for Beginners

I’ve shared detailed information about seven different apps. I’ve explained what makes each one useful. I’ve shown you how to choose based on your needs. But here’s the most important thing I can tell you: stop researching and start acting.

The perfect app doesn’t exist. The app that works for your friend might not work for you. The app that seemed perfect in theory might not fit your actual life. The only way to know is to pick one and use it for 30 days.

Download an app today. Spend 20 minutes setting it up. Check it every morning for a month. After 30 days, decide whether it’s helping. That’s the actual path to better financial management. Not endless research. Not comparing spreadsheets of features. Just action.

Budgeting becomes natural when your money is visible. When you see your complete spending picture. When you know exactly what’s happening with your finances. AI budgeting apps make that visibility possible without requiring hours of manual work.

Your first step is picking one app and opening it. Which one will it be?

Related Reading

You can also read our complete guide on how to use AI to manage money and save more to learn step-by-step strategies and proven methods that complement these app choices.

Comments (2)

13 Best Conversational AI Tools for Real Estate Agents 2026says:

June 5, 2026 at 7:29 pm[…] using AI budgeting apps to log time savings and deal values helps quantify true ROI. Our guide to best AI budgeting apps includes tools that track business metrics alongside personal finance, helping you measure […]

Best AI Tools for Investment Research: 25+ Platforms for 2026says:

June 15, 2026 at 8:28 pm[…] Before diving into AI investment tools, consider building a solid financial foundation using the best AI budgeting apps for beginners in USA, which can help you allocate capital for investing and track where your money is […]