Managing money in 2026 feels harder than ever before. Rising costs are eating into your paycheck, you’re juggling multiple bank accounts and subscriptions, and traditional budgeting methods seem outdated. You probably know you should be saving more, but between work stress and financial complexity, it feels overwhelming. The reality is that manually tracking every dollar is no longer practical in today’s world. You need something smarter, something that works while you sleep.

Here’s what’s interesting: 78% of Americans now use AI financial tools to manage their money. That statistic alone tells you something important. AI has quietly become mainstream in personal finance, and it’s delivering real results for millions of people. Yet most people still don’t know how to use AI to manage money and save more effectively. They download an app, get overwhelmed by options, and either abandon it or use it passively without seeing real benefits.

The difference between people who succeed with AI money management and those who don’t comes down to one thing: having a clear process. AI removes friction from financial management automatically. Instead of asking “How much did I spend last month?” AI answers “How much will I spend next month?” It doesn’t just record your transactions; it learns from them. It identifies spending patterns you’d never notice manually. It spots that $180 per month disappearing to unused subscriptions. It predicts financial problems before they happen. Most importantly, it does all this without requiring hours of your time.

By the end of this guide, you’ll have a step-by-step process to implement AI money management in your life. You’ll understand which tools actually work, how to set them up properly, and the five specific strategies that create real savings. You won’t need technical skills or financial expertise. You’ll discover how to go from financially stressed to financially confident in just 30 days. This article covers everything from choosing the right AI tool to implementing five proven savings strategies to tracking your progress and celebrating wins.

Let’s dive into how to use AI to manage money and save more in 2026.

Understanding AI in Money Management

When people hear “AI money management,” they often imagine robots controlling their finances or complex algorithms they can’t understand. The reality is much simpler and more practical.

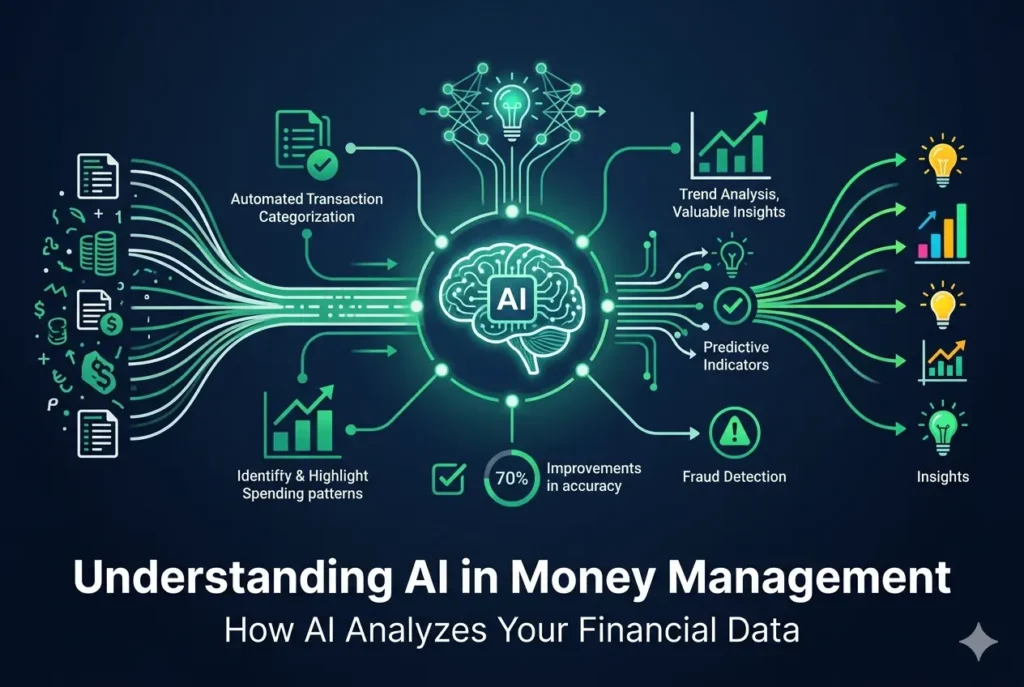

AI money management is about smart software that learns from your financial data. It analyzes your transactions, spending habits, and financial goals, then provides personalized guidance based on your unique situation. Think of it as having a financial assistant that works 24/7, never takes breaks, and gets smarter every time you use it.

So what does AI actually do with your money? First, it automatically categorizes your transactions. Instead of manually sorting purchases into categories like “groceries,” “entertainment,” or “subscriptions,” the AI does this instantly. As you use it, the system learns your patterns and gets better at accuracy. Second, AI identifies trends you’d miss on your own. It spots that you spend more on dining after stressful workdays. It notices your subscription costs have doubled in six months. It detects unusual transactions that might indicate fraud. Third, AI predicts your future spending. Rather than just showing what you spent last month, it forecasts what you’ll likely spend next month based on historical patterns, seasonal trends, and upcoming obligations. Fourth, AI provides personalized recommendations specifically for your situation, not generic advice for everyone.

How does this differ from traditional budgeting tools? Old-school apps require manual entry and categorization. They show you historical data, which is useful but limited. Generic budgeting advice doesn’t account for your unique situation, habits, or goals. Modern AI tools handle everything automatically, predict your future instead of analyzing your past, and customize recommendations based on your actual behavior. This shift from reactive to proactive money management changes everything.

Why does this matter in 2026? The economic reality has shifted. Inflation is eating into savings faster than ever. Your financial life is more complex, with multiple accounts, subscriptions, and income sources. Manual tracking doesn’t scale. The good news is AI technology has matured significantly. It’s no longer experimental. Millions of Americans have successfully implemented AI money management and achieved real results.

Pre-Implementation: Setting Your Foundation

Before you download anything or connect any accounts, you need to prepare. This foundation work takes just an hour but determines your success.

Start by defining your primary goal. Different people use AI for different purposes. Some want budget control and spending awareness, desperate to finally know where their money goes. Others focus on savings automation, wanting to build wealth systematically. Some need to eliminate debt faster. Others want to reduce expense waste, especially those subscription drains. A few seek investment optimization. Understanding your primary goal matters because it determines which tool you’ll choose and how you’ll use it.

Next, assess your current situation honestly. Create a simple inventory of all your accounts: checking, savings, credit cards, investment accounts. Review your last three months of spending. What are your total monthly expenses? What’s your biggest financial pain point right now? Are you living paycheck to paycheck? Do subscriptions drain your account regularly? Can’t save anything consistently? This baseline helps you measure progress later.

Identify your key problem. What frustrates you most about your current finances? Is it not knowing where money goes? Is it inability to save? Are subscriptions the villain? Is your spending out of control? Different problems benefit from different strategies. Solving your biggest problem first creates momentum and confidence.

Finally, commit to the process with clear expectations. Initial setup takes about 30 minutes. Daily engagement requires just 5-10 minutes. Weekly reviews take 15 minutes. You’ll see first results in 2-4 weeks. Realistic expectations prevent quitting when you don’t see instant magic.

Step-by-Step Implementation Process

This is where the real action happens. Follow these phases exactly.

Phase 1: Choosing Your AI Tool

You have several tool types available. Budgeting-focused apps like YNAB and Copilot Money work best if you want complete spending control. Conversational AI assistants like Cleo appeal to people who prefer a chat-based interface and friendly approach. Comprehensive dashboards like Monarch Money shine for couples managing shared finances. Subscription trackers like Rocket Money specifically target expense waste. Investment-focused platforms like Empower and Betterment handle wealth building and optimization.

How do you choose? Match the tool to your primary goal from earlier. Consider your comfort with technology. Check if free trials are available. Read recent 2026 reviews. Most importantly, start with just one tool. Don’t overthink it. You can always switch later if needed. The critical factor is picking something you’ll actually use.

Here’s what I recommend based on different situations. Beginners should start with Cleo or PocketGuard because they’re approachable and simple. Couples managing joint finances do best with Monarch Money. People serious about budgeting discipline choose YNAB. Anyone wanting everything in one place should try Copilot Money. Those frustrated with subscriptions specifically benefit from Rocket Money.

Phase 2: Initial Setup

Setup takes three hours spread across the first week. Hour one involves downloading and creating your account. Go to the tool’s website or app store. Download the app or open the website. Create an account using your email. Verify your email confirmation. Set a strong password. Complete your basic profile. This takes about 10 minutes and gives you access immediately.

Hour two means connecting your bank account. Open the banking section within the app. Select your primary checking account. Authorize the connection securely. Verify the account appears correctly and shows recent transactions. Don’t connect everything today. Just start with your main checking account. This takes 15-20 minutes.

Hour three involves reviewing and configuring. Look at your last 30 days of transactions. Review how the AI categorized them. Correct obvious mistakes. The tool learns from your corrections and improves over time. Set up a basic budget if desired. Create one savings goal. Enable key features like spending alerts, unusual activity notifications, and cash flow forecasting if available. This takes 20-30 minutes.

Days two through seven are about building habit. Check the app for five minutes daily. Review insights and alerts. Answer any categorization questions. Notice patterns emerging. Look for opportunities to improve. Build familiarity with the interface. Making this a habit during the first week determines long-term success.

Phase 3: Activation and Optimization

Week two means deeper analysis. Review two to three months of spending history. Look for patterns the AI identifies. What are your top three spending categories? Spot waste and unnecessary expenses. Find forgotten subscriptions, which is especially important. Identify emotional spending triggers. Review all AI recommendations. Start planning changes based on your findings.

Week three is implementation time. Cancel identified unused subscriptions. Average savings here is $60-150 monthly. Set up automatic savings transfers. Even $50 per week becomes $2,600 per year. Create specific savings goals like emergency funds or vacation funds. Adjust budget categories if needed. Enable additional account connections if you’re ready. Test the predictive features.

By week four, measure and evaluate. Have you saved more than before? Do you understand your spending better? Did you find and eliminate waste? Is this becoming automatic? Are insights actually helping your decisions? Answer honestly. If yes, keep going and add more tools or strategies. If no, switch tools and try again.

Going forward, review weekly for 15 minutes. Reassess goals monthly. Analyze spending patterns quarterly. Complete a full financial audit annually. Add secondary tools when the first becomes routine. Build on early success.

Practical Strategies to Actually Save More

Understanding how to use AI to manage money matters less if you don’t act on it. These five specific strategies create real results.

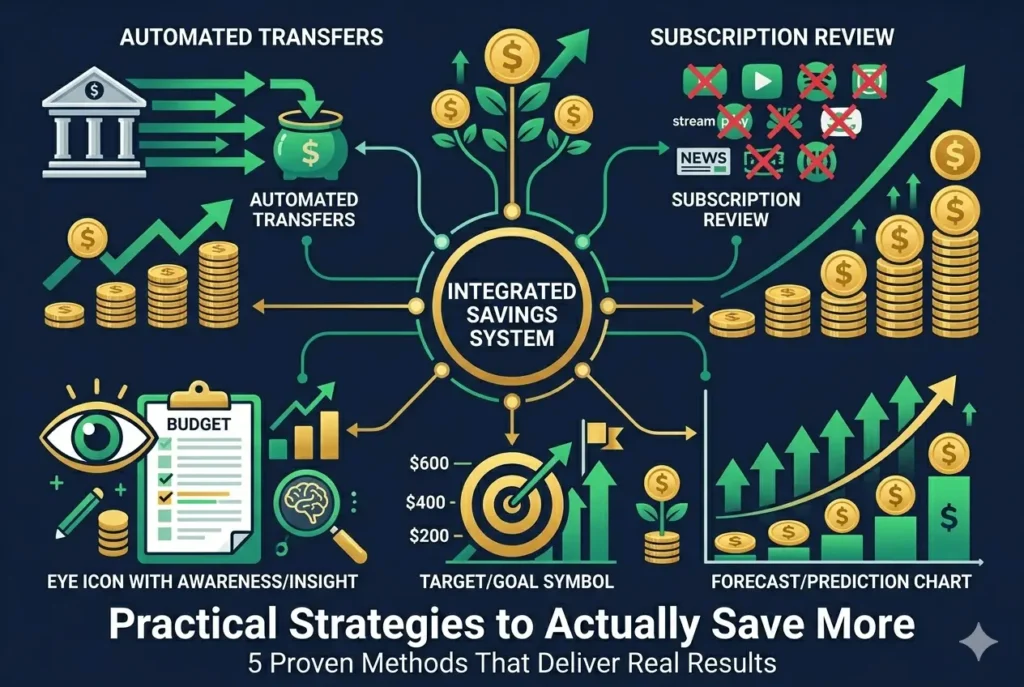

Strategy 1: Automated Savings

This is the single most effective savings method because it removes willpower from the equation. You don’t need discipline when the system handles it automatically. Set up an automatic transfer from checking to savings on payday, before you have a chance to spend the money. Even $50 weekly becomes $2,600 annually. Your brain adjusts to living on less because you never see the money. Eighty percent of people who implement automated savings stick with it long-term.

To implement: Choose your target amount, set up the automatic transfer, schedule it for payday, then forget about it. Done.

Strategy 2: Subscription Elimination

The average person pays for 5-10 unused subscriptions. That’s $40-150 monthly disappearing. AI tools identify these automatically. The strategy is simple: cancel what you don’t use. One hour of work creates ongoing savings for the rest of the year. Average savings run $60-150 monthly or $720-1,800 annually.

To implement: List all subscriptions you’re paying. Mark anything unused in 30 days. Cancel those immediately. Set a quarterly reminder to review again.

Strategy 3: Spending Awareness

Simply seeing spending patterns changes behavior. People reduce discretionary spending 15-25% just from awareness. AI makes patterns visible automatically. No restriction needed. Behavioral change happens naturally when you understand your habits.

To implement: Check the app daily for five minutes. Look for trends. Review categories weekly. Notice what surprises you.

Strategy 4: Goal-Based Budgeting

Restrictive budgets feel punishing. Goal-based budgeting feels empowering. Instead of “you can only spend $50 on dining,” it’s “you’re saving $1,000 for your emergency fund by month three.” AI shows progress visually. Specific targets keep you focused. People achieve goals 40% more often when using this approach.

To implement: Create specific goals with timelines. Track progress visually. Celebrate milestones. Review monthly.

Strategy 5: Predictive Spending Adjustment

AI predicts your month-end balance before the month ends. You see problems coming. You can adjust spending proactively. Zero overdraft fees. Financial stability improves dramatically. Peace of mind is the real reward.

To implement: Enable cash flow forecasting. Check projected month-end balance weekly. Adjust spending if forecast looks low. Prevent problems before they happen.

Real Results People Achieve

These aren’t hypothetical benefits. Real people achieve real results.

A paycheck-to-paycheck professional felt constantly broke despite decent income. No emergency savings. Financial anxiety constant. She implemented an AI budgeting app. Discovered $180 monthly in unnecessary subscriptions. Set up $100 weekly automatic savings. After three months, she’d saved $1,300 and started an emergency fund. Now she feels in control instead of overwhelmed.

A couple managing joint finances experienced constant money arguments. No visibility into household spending. They used a shared AI dashboard. Discovered $240 monthly in duplicate spending. Set joint goals. Now they save an additional $300 monthly together. Money arguments decreased 70%. They finally align on financial priorities.

A self-employed freelancer couldn’t budget with irregular income. Boom and bust cycles made planning impossible. She used an AI app that adjusted automatically to income patterns. Could predict tight cash flow periods. Adjusted spending proactively. Eliminated the financial roller coaster. Consistent savings despite irregular income. Real peace of mind.

An optimization-focused individual already had good habits but wanted more. AI identified $150 monthly in small waste items. Optimized tax strategies. Found subscription savings. Added $2,000 yearly in savings from optimization alone.

An overwhelmed parent juggled multiple accounts and complex family finances. No unified view. Family financial stress and tension. AI provided unified visibility. Better communication with spouse. Reduced family financial stress. Saves $200 monthly as a family.

Common thread: Initial setup takes 30-60 minutes. Results appear within 30 days. Long-term benefit transforms the financial relationship with money. Tool cost of $5-15 monthly is recovered in savings alone. Return on investment is immediate and ongoing.

Common Mistakes to Avoid

Most failures don’t come from lack of information. They come from avoidable mistakes.

Mistake one is starting with too many tools simultaneously. Multiple apps create confusion. Login fatigue leads to abandonment. Information overload paralyzes action. Solution: Start with one tool. Give it three months. Add a second tool only if the first is thriving. Quality engagement beats quantity. Single-tool users succeed 80% of the time.

Mistake two is unrealistic expectations. People expect instant massive savings. Expect AI to replace human judgment. Demand perfection immediately. Quit when month-one savings are only $75 instead of $500. Reality: First month typically yields $50-150. Month three shows meaningful transformation. Month six shows life-changing results. AI suggests. You decide. Celebrate small wins. Meaningful change takes three to six months.

Mistake three is not reviewing regularly. Set it and forget it doesn’t work. Tools work best with engagement. Missing opportunities happens silently. You never see the benefits if you don’t look. Solution: Weekly 15-minute reviews minimum. Make it part of your routine. Daily five-minute check-ins. Habit formation is key. Weekly reviewers save twice as much as passive users.

Mistake four is ignoring data privacy. Connecting to unknown apps risks financial data security. Poor privacy policies exist. Unverified platforms are dangerous. Solution: Only use well-known, established platforms. Check for security certifications. Read privacy policies. Stick with trusted, verified brands. Established platforms have strong security.

FAQ: Your Burning Questions Answered

How long before I see real savings?

First results appear in 1-2 weeks through awareness. Meaningful results accumulate by month three. Transformative results happen by month six as habits change automatically.

Is it too late to start?

No. Starting today means more time for compound savings. Even starting one year from now beats never starting. The best time is always today.

Which tool is best?

It depends on your specific goals. Try free versions first. Copilot Money works well for complete overviews. YNAB excels for budgeting discipline. Cleo provides simplicity and approachability. Monarch Money suits couples specifically.

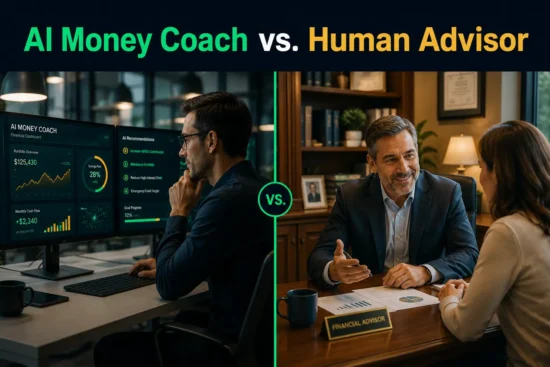

Will AI replace my financial advisor?

No. AI handles routine management and optimization beautifully. Humans are essential for complex decisions, major life changes, tax strategy, and big financial planning. They complement each other perfectly.

How much time does this take?

Initial setup takes 30 minutes. Daily engagement requires 5-10 minutes. Weekly reviews take 15 minutes. That’s minimal time for major results compared to manual tracking.

Is my financial data safe?

Yes, if you use reputable tools with encryption and security certifications. Check security badges. Read privacy policies. Avoid unknown apps. Established platforms have excellent security measures.

Can I use AI and still work with a financial advisor?

Absolutely. AI handles day-to-day management. Advisors handle strategy. No conflict. Many professionals recommend both together.

What if I have irregular income?

AI handles this exceptionally well. Use percentages instead of fixed amounts. AI adjusts automatically to your unique income patterns. Freelancers and self-employed people benefit greatly.

How much can I realistically save?

Realistic range is $100-300 monthly from combining strategies. Some save more. Some save less. Every situation is unique. Your goal determines your savings potential.

What if I fail or quit?

Start again. No harm in trying, switching tools, or taking breaks. Progress matters more than perfection. Most people succeed on their second attempt.

Getting Started Today

The biggest barrier to success is overthinking. Here’s your simple path forward.

Right now, in the next 30 minutes, choose your tool from recommendations above. Create an account. Download the app or access the website. Connect your checking account. Review the basic setup. That’s it. Done.

Today, over the next two to three hours, review your last 30 days of transactions. Correct AI categorization errors. Set one financial goal. Enable key features like alerts and budgets.

This week, check the app daily for five minutes. Look for patterns. Make one small change based on what you find. Tell someone you’re doing this for accountability.

This month, act on major findings. Cancel unused subscriptions. Set up automatic savings transfers. Review progress mid-month. Adjust as needed.

The real key is consistency over intensity. Small actions compound. Thirty days provides real value. After that, it becomes automatic. Results accelerate over time. New financial habits form naturally. Financial stress decreases noticeably. Savings accumulate steadily.

Conclusion: Your AI-Powered Financial Future

Let’s recap what you’ve learned. AI transforms money management from reactive to proactive. Seventy-eight percent of Americans already use AI financial tools successfully. Setup takes just 30 minutes. It delivers years of value. Average person saves $100-300 monthly. Tool costs are recovered in savings alone.

But this isn’t really about making more money. It’s about managing what you have better. Seeing your money clearly. Reducing financial stress dramatically. Building actual wealth systematically. Preventing financial emergencies before they happen. Gaining control and peace of mind.

The 2026 reality is significant. A gap is widening between people using AI and those not using it. Non-users leave thousands on the table annually. Users build wealth systematically. AI-powered money management is becoming essential, not optional, for financial health.

You have a choice. You can continue managing money manually, getting stressed about subscriptions, never knowing where money goes, feeling overwhelmed. Or you can leverage AI and save thousands while reducing financial stress. The decision is yours.

You don’t need to be tech-savvy. Tools are designed for regular people. Start today, not tomorrow. Results appear faster than expected. Financial freedom is more achievable than you think. Your future self will thank you.

Pick one tool. Set it up today. Give it 30 days. Measure the results. You’ll be surprised at what changes when you finally have visibility and automation handling your finances.

The only question is: Will you start today?

Comments (1)

Best AI Budgeting Apps for Beginners in USA: Complete Guide to Smart Money Management in 2026 - Trendoutsidersays:

May 24, 2026 at 10:07 pm[…] apps are designed differently than traditional money management tools. They learn from your spending patterns. They automatically categorize your transactions instead of […]