Introduction

A financial advisor costs $200 to $300 per hour. An AI money coach costs $25 per month or free if you’re willing to use ChatGPT. But which one actually helps you build wealth?

I’ve spent the last year testing both. I’ve sat through $500 financial advisor consultations and set up a free ChatGPT money coach that caught spending patterns the paid app missed. I’ve also talked to dozens of people caught between the two options, uncertain whether they should invest in professional advice or trust an algorithm with their money.

Financial coaching is valuable. The data shows that people who work with coaches are more likely to reach their goals, save consistently, and build lasting wealth. But coaching is also expensive and inaccessible. Most people can’t justify $150 to $300 per hour, especially when they’re starting out with small amounts to invest or struggling with debt.

That’s where AI money coaches enter the picture. They promise 24/7 personalized guidance for a fraction of the cost. No waiting for appointments. No judgment. No minimum account size. But hype and reality are different things. An AI money coach isn’t a replacement for human expertise in every situation.

Here’s the truth: Neither AI nor human advisors are universally better. The right choice depends on your situation, your goals, your budget, and your comfort level with technology. Some people need both.

This guide walks you through what each option actually does, how they compare across cost, accessibility, and personalization, and how to choose based on what you’re trying to accomplish.

What Is an AI Money Coach?

An AI money coach is a financial guidance system powered by large language models (like GPT-4 or Claude) or specialized fintech AI trained on financial data and coaching principles. It’s not a chatbot that answers random questions. It’s a system designed specifically to help you make smarter money decisions.

How an AI Money Coach Works

Here’s what happens under the hood. Most AI money coaches connect to your bank account through secure APIs like Plaid, or you manually input your financial information. The system then categorizes your transactions, identifies patterns in your spending, and compares your behavior to benchmarks (how much does the average person in your income bracket spend on dining out?).

When you describe your financial goals in natural language (I want to pay off my credit card or I’m saving for a house), the AI uses natural language processing to understand what you’re actually asking. It generates personalized recommendations based on your specific income, expenses, and habits. It tracks your progress over time and adjusts recommendations as your situation changes.

The AI gets smarter the more you interact with it. Early recommendations are generic (save 20 percent of income). After weeks of interaction, they become specific to your behavior (based on your pattern of overspending on Thursdays, you should build in a $50 buffer each week for discretionary spending).

What AI Money Coaches Actually Do

They analyze your income, expenses, and financial goals. They track spending patterns and identify inefficiencies. They suggest budgeting strategies based on your specific habits. They recommend debt payoff strategies (avalanche versus snowball methods). They help you set realistic savings targets. They provide real-time alerts and behavioral nudges before you spend money you shouldn’t. They answer financial questions on demand. They run what-if scenarios (if I save an extra $200 per month, how fast will I hit my goal?).

This sounds comprehensive, but there’s an important caveat.

What AI Money Coaches Cannot Do

They don’t provide tax advice (they’re not licensed to do so). They don’t manage your investments directly. They don’t handle complex situations like estate planning, divorce finances, or business-related tax strategy. They don’t make subjective judgments about your life priorities. They can’t explain the deeper emotional reasons behind your spending patterns. They don’t adapt to life changes unless you explicitly tell them about them.

If you inherit $500,000 but forget to update your financial profile, the AI continues recommending the same modest savings strategy. If you lose your job and don’t change your income information, the budget advice becomes irrelevant overnight.

Types of AI Money Coaches

Embedded coaches like Stash’s Money Coach or SoLo IQ are built into existing fintech platforms with access to your real account data. Standalone apps like MoneyCoach and Sorted are apps you download that connect to your bank via API. DIY coaches like ChatGPT or Claude are systems you set up yourself using prompts, and you manually share your financial information. B2B platforms like Kiro Money are infrastructure that financial companies embed into their products (not available to consumers directly).

Each type has different strengths. Embedded coaches know your entire financial picture because they’re connected to your account. Standalone apps offer more privacy because they don’t store your account directly. DIY coaches offer customization and privacy but require more work from you.

What Is a Human Financial Advisor?

A human financial advisor is a person licensed and trained to give financial guidance and manage investments. But not all advisors are created equal, and understanding the types matters.

Types of Human Advisors

Certified Financial Planners (CFPs) are licensed professionals who typically charge $150 to $300 per hour or 1 percent of your assets under management. They provide holistic planning, are regulated by professional standards, and are required to complete specific education and ethics training. Fee-only advisors charge by the hour or with a fixed fee and earn no commissions. They’re more aligned with your interests because they don’t benefit from selling you specific products. Cost: $100 to $300 per hour.

Commission-based advisors earn money when they sell you investment products. The consultation is often free, but there’s a potential conflict of interest because they benefit from recommending certain products. You see these at banks and brokerage firms. Robo-advisors are a hybrid: algorithms manage your investments, and you have some access to human advisors if needed. Cost: 0.25 to 0.75 percent of your assets annually.

Financial coaches (not advisors) are not licensed like CFPs, but they focus on behavioral coaching and building financial habits. They’re often cheaper ($50 to $150 per hour) and less regulated. They’re useful for people who need accountability and behavioral support, not investment management.

What Human Advisors Do That AI Cannot

They ask probing questions about your values and life priorities. A good advisor doesn’t just ask what you want to save, they ask why it matters, what wealth means to you, and what would make you feel financially secure. They understand complex life situations like divorce, inheritance, and business sales. They provide tax-optimization strategies based on your specific situation, not generic benchmarks. They manage investments directly and rebalance your portfolio as markets change. They review contracts and complex financial documents. They provide emotional accountability and support during stressful periods. They make judgment calls in ambiguous situations. They build a long-term relationship and adjust strategy as your life changes.

This is what you’re paying for with a human advisor: not just financial knowledge, but judgment, experience, and relationship.

The Hidden Costs of Human Advisors

The monetary costs are obvious. $150 to $300 per hour adds up fast. For someone with $100,000 to invest, a 1 percent annual fee equals $1,000 per year forever. But there are hidden costs too.

There’s an emotional cost. You might feel judged or ashamed discussing your financial mistakes. A good advisor creates a judgment-free environment, but not all do. There’s the time cost. You have to schedule calls, prepare information, and attend reviews. There’s the conflict-of-interest risk. Even fee-only advisors might recommend higher-margin products or more frequent trading to justify their fees. There’s the accessibility barrier. Many advisors have minimum account sizes ($250,000 or more). If you have less, you’re locked out.

AI Money Coach vs. Human Advisor: Side-by-Side Comparison

Let me be direct about what matters most: cost, accessibility, personalization, and what each can actually accomplish.

Comparison Table

| Factor | AI Money Coach | Human Advisor |

|---|---|---|

| Cost | $25-100/month (app) or free (DIY ChatGPT) | $150-300/hour or 1% of assets annually |

| Availability | 24/7, instant | Office hours, need to schedule |

| Personalization | Pattern-based from your data | Relationship-based, subjective judgment |

| Complexity handling | Simple budgeting, debt payoff | Complex tax, estate, business situations |

| Tax advice | No (not licensed) | Yes (if CFP) |

| Investment management | No | Yes |

| Accountability | Nudges and reminders | Regular check-ins, relationship pressure |

| Setup time | Minutes to hours | Days to weeks |

| Data privacy | Varies by platform | Your data stays with advisor (regulated) |

| Emotional support | Limited (algorithm doesn’t care) | Can provide comfort and perspective |

| Minimum account size | None | Often $100K-$250K+ |

| Learning curve | Low if app is intuitive | Varies by advisor’s communication style |

Cost-Benefit Analysis

An AI coach’s cost is predictable and low. $25 to $100 per month won’t break your budget. The benefit is real-time, personalized guidance whenever you need it. The ROI is high if you actually implement the recommendations.

A human advisor’s cost is high but may be justified if your situation is complex. $150 to $300 per hour or 1 percent of assets annually adds up, but you’re paying for expertise that has taken years to develop. The ROI depends on advisor quality and the complexity of your situation. If you have simple finances and basic goals, you’re overpaying.

Understanding the bigger picture of 17 best AI tools to make money in 2026 helps you see how financial guidance tools fit into your overall wealth-building strategy beyond just coaching and advice.

Accessibility

An AI coach is always available. No minimum account size. No bias against small investors. No judgment. You can check in at 2 AM if you’re having a moment of doubt about a purchase.

A human advisor has office hours. Minimum account sizes lock out people who don’t have significant assets. They may be judgmental, consciously or not. But if they’re a good fit, the relationship becomes a valuable part of your financial life.

Depth of Personalization

AI personalization is based on your data and patterns. It’s personal in the sense that it knows your spending habits, income, and stated goals. But it’s generic for situations outside that data. If something unexpected happens (you inherit money, face a major life change, have an unusual income scenario), the AI lacks context to give meaningful advice.

Human advisor personalization is relationship-based. Through conversations, they understand your values, your fears, your priorities, and your unique circumstances. They can adapt to unexpected situations through judgment. But this takes time and depends on the quality of the relationship.

Accuracy and Reliability

AI is accurate for simple, common situations. If you’re asking about standard budgeting strategies or typical debt payoff approaches, the AI will give reliable advice. But AI can hallucinate. If you ask “Should I refinance my mortgage?” the AI might generate credible-sounding advice without access to current rates or your specific loan terms. It’s unreliable for novel or complex situations. And importantly, AI coaches aren’t liable if their advice causes financial harm.

Human advisors are regulated and can be held liable if their advice causes harm. But human judgment is also fallible. It depends entirely on the advisor’s quality, experience, and ethics.

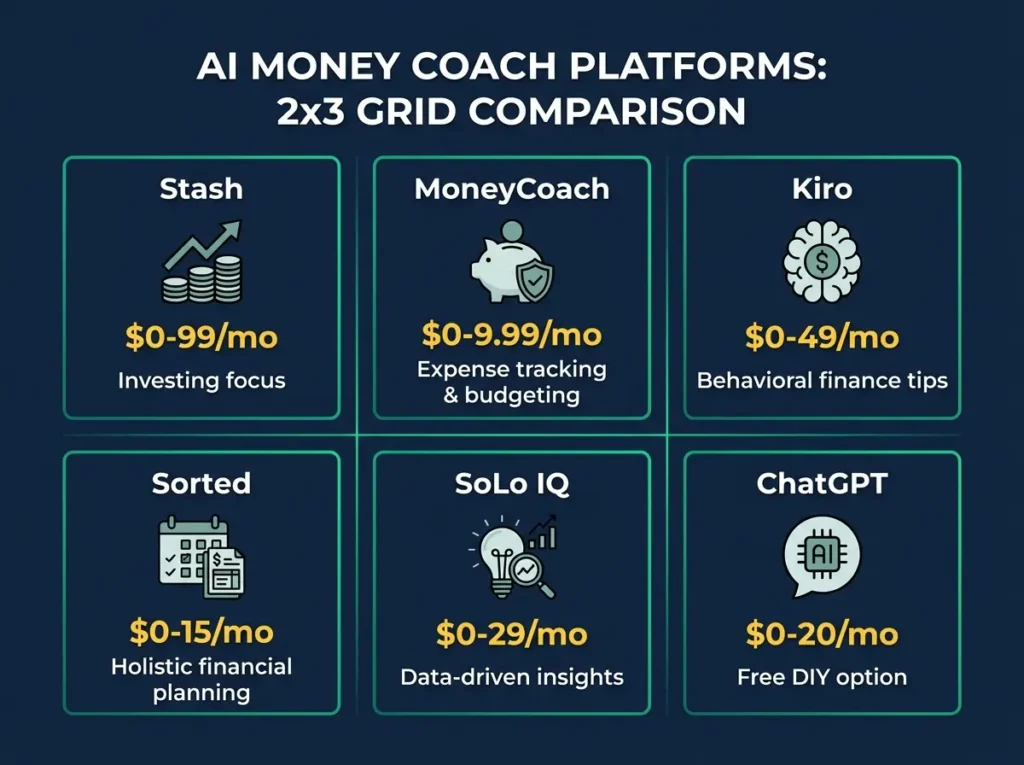

Six Leading AI Money Coach Platforms Reviewed

You have options. Let me walk through the real platforms people are using.

1. Stash AI Money Coach (Embedded in Stash App)

What it is: AI-powered financial guidance built directly into Stash’s investment and budgeting app.

Key features: It’s connected to your real Stash account, so it understands your investments, spending, and goals. You get 24/7 conversational guidance on budgeting, investing, and retirement planning. The insights are personalized based on your actual activity. It helps with goal-setting and progress tracking. It sends real-time alerts if you’re about to overspend.

Best for: Beginners who want investing, budgeting, and coaching in one platform.

Cost: Included in your Stash subscription ($0 to $99 per month depending on tier).

Strengths: It’s integrated (it knows your real money), backed by a trusted brand, and excellent for beginners.

Limitations: It only advises on money within Stash (if you have accounts elsewhere, it can’t see them). The AI is competent but not cutting-edge. It’s focused on investing, with less emphasis on debt payoff.

2. MoneyCoach (Standalone App)

What it is: Personal finance app (iOS, Mac, Apple Watch) with AI-assisted budgeting.

Key features: Expense tracking and automatic categorization. Personalized budget recommendations. Multi-currency support (good if you have money internationally). Cross-device sync. Goal planning and tracking. Detailed reports on your spending.

Best for: People who want a simple, elegant budgeting app with light AI assistance.

Cost: $4.99 per month or $39.99 per year.

Strengths: The interface is beautiful. It’s affordable. No account minimums. Works offline.

Limitations: It’s less conversational than other AI coaches. It’s more app-with-smart-suggestions than true coaching. Limited investing features.

3. Kiro Money (B2B Platform)

What it is: White-label AI financial coaching platform that financial companies embed into their products. You won’t use this directly.

Key features: Personalized real-time guidance. Behavioral nudges. Goal tracking and adjustment. Investment guidance based on risk tolerance. Data-driven recommendations using bank connections.

Best for: Financial companies, banks, and fintech platforms (not available to consumers directly).

Cost: Enterprise pricing (custom quotes).

Strengths: Enterprise-grade security. Compliance-ready. Deep data integration. Proven at scale.

Limitations: Not available to average consumers. Expensive. Overkill if you only need budgeting help.

4. Sorted (Mobile-First AI Coach)

What it is: Gen Z-focused AI money coach app centered around a daily spend number.

Key features: Every morning, Sorted tells you one number: what you can spend today without breaking your plan. A conversational AI coach gives direct advice (“Skip the latte, pay the card first. Yes, get the sushi”). Real-time coaching on purchase decisions in the moment. Debt payoff strategies. Goal tracking for side hustle income and debt crushing.

Best for: Young people, side hustlers, people with irregular income trying to stay on budget.

Cost: Free trial (14 days), then $14.99 per month or $99 per year.

Strengths: Conversational and directive (it tells you what to do). Built specifically for Gen Z. Excellent for debt payoff focus. Uses GPT-4 and Claude under zero-retention agreements.

Limitations: Limited investing features. Newer company means less track record. No multi-currency support.

5. SoLo IQ (Personalized Financial LLM)

What it is: AI financial coach from SoLo Funds, built on data from billions of transactions across their community lending platform.

Key features: Hyper-personalized guidance that understands your transaction history at a deep level. Conversational AI interface. Cash flow prediction. Spending behavior analysis. Budget recommendations grounded in your actual spending, not averages.

Best for: People who want AI that truly understands their financial reality based on massive real-world data.

Cost: Free to use as a SoLo Funds member.

Strengths: Exceptional personalization trained on 1 billion transactions. Real-world grounded (not based on theory). Behavioral insights. Community connection.

Limitations: Only available to SoLo Funds members. Focused on their lending aspect. Less suitable if you don’t need community lending.

6. ChatGPT as DIY AI Money Coach (Free or $20/Month)

What it is: You create a custom ChatGPT project and give it your financial information manually.

Key features: Completely customizable (you set the rules and coaching style). Free (ChatGPT free tier) or $20 per month (ChatGPT Plus). Conversational and adaptive. Can handle complex what-if scenarios. You control what information you share.

Best for: Tech-comfortable, budget-conscious people who want a custom setup. People uncomfortable sharing data with fintech companies.

Cost: Free or $20 per month for ChatGPT Plus.

Strengths: Highly customizable. Cheapest option. No data collection by third parties. Surprisingly good at financial reasoning.

Limitations: You have to manage it yourself (no automation). Manual data entry is tedious. No bank integration. Less personalized than apps unless you feed it lots of data.

Use-Case Recommendations: Which Should You Choose?

Stop trying to find the universal best option. There isn’t one. The right choice depends on what you’re actually trying to accomplish.

If Your Main Goal Is Budgeting and Spending Control

Use an AI money coach (app or ChatGPT DIY).

Why: AI excels at pattern recognition. It can categorize spending, identify leaks, and suggest realistic limits in minutes. A human advisor isn’t necessary here. You’re paying for expertise you don’t actually need.

Implementation: Start with Sorted ($14.99 per month) if you want conversational guidance. Start with ChatGPT ($0 or $20) if you’re tech-comfortable and budget-conscious.

Timeline: You’ll see spending insights in 2 to 4 weeks.

If Your Main Goal Is Paying Off Debt

Use an AI money coach (Sorted or ChatGPT DIY), optionally with a human financial coach.

Why: AI can map out avalanche versus snowball strategies, run what-if scenarios (if I pay an extra $100 per month, I’m debt-free in X months), and provide real-time encouragement. A human financial coach adds emotional accountability and can help if your situation is complex (multiple income sources, income instability, or high-stakes debt like bankruptcy risk).

Implementation: Start with Sorted for daily accountability. If debt is high-stakes, add a human financial coach ($50 to $150 per hour).

Timeline: AI provides immediate guidance. Payoff timeline depends on your income and debt amount.

If Your Main Goal Is Investing and Long-Term Wealth Building

Use a human financial advisor (CFP) or robo-advisor hybrid.

Why: Investing is complex. You need guidance on asset allocation, diversification, tax-loss harvesting, rebalancing, and long-term strategy. AI can suggest generic advice (diversify), but it can’t optimize your specific situation. A human CFP or robo-advisor with human access is better.

For research-focused investors, reviewing best AI tools for investment research can enhance your analysis, though professional advisors still manage the actual allocation and rebalancing.

Implementation: If you have $25,000 to $100,000, use a robo-advisor (Vanguard Personal Advisor Services costs 0.3 percent annually plus human advisor access). If you have $100,000 or more, hire a CFP ($200 to $300 per hour or 1 percent of assets annually).

Timeline: Setup takes weeks. Strategy development takes 1 to 3 months.

If Your Financial Situation Is Unusual or Complex

Use a human advisor (CFP or financial coach) first, then optionally add AI for daily support.

Why: Complex situations require judgment. Variable income (freelancer, business owner), tax complications, unexpected inheritance, major life change (divorce, health crisis, job loss). These situations need human judgment that AI can’t provide.

If you’re exploring ways to handle your complex income situation, understanding 100 ways to make money with AI might reveal opportunities, but a CFP is still essential for structuring complex financial scenarios.

Implementation: Hire a CFP for a one-time or quarterly consultation ($2,000 to $10,000 per year). Use an AI money coach in between for daily support and simple decisions.

Timeline: Initial consultation takes 1 to 2 weeks to schedule. You’ll get recommendations in 2 to 4 weeks.

If You’re Budget-Conscious and Tech-Comfortable

Use ChatGPT DIY money coach or Sorted.

Why: You save $200+ per year compared to human advisors. You get conversational support without data privacy concerns (if using ChatGPT). You control the setup.

For a comprehensive understanding of free AI tools for marketing and other free AI resources, you’ll see that ChatGPT is also a powerful free option for personal financial coaching with zero cost.

Implementation: Set up ChatGPT Money Coach in a custom project ($0 to $20 per month for ChatGPT Plus). Takes 30 minutes. Feed it your financial information manually as you check in. Use it for daily budgeting questions, what-if scenarios, and accountability.

Timeline: Setup is immediate. You get guidance the same day.

If You Want Behavioral Change (Building Better Money Habits)

Use a hybrid: AI money coach (for real-time nudges) plus human financial coach (for accountability).

Why: Real behavioral change happens through repeated small decisions and emotional support. AI provides real-time nudges (That $7 latte impacts your goal) right before you spend. A human coach provides accountability and helps you understand why you make certain decisions.

The concept of building better habits ties into AI and productivity tools that save time, because financial discipline itself is a productivity habit that frees up mental energy and time.

Implementation: Use Sorted or Whistl ($15 to $25 per month) for real-time behavioral coaching. Hire a financial coach for monthly or quarterly check-ins ($50 to $150 per hour or $200 to $500 per month retainer).

Timeline: You’ll start seeing behavioral shifts in 4 to 8 weeks.

When AI Money Coaches Fail (Limitations and Risks)

I want to be honest about where AI money coaches don’t work. This is where trust is built.

Technical Limitations

AI can hallucinate financial facts. You ask “Should I refinance my mortgage?” and the AI generates credible-sounding advice without access to current rates or your loan terms. The advice sounds authoritative but is actually made up.

AI is pattern-based. If your situation is outside the typical pattern (huge one-time income, unexpected major expense, job loss, disability), AI struggles. It doesn’t know how to handle situations it hasn’t seen in training data.

AI is limited to financial data. It doesn’t know your values, family situation, health status, or dreams. It can’t tell you whether a house purchase aligns with your life goals. It can suggest you save money, but it can’t evaluate whether you should spend it on something that matters deeply to you.

Privacy and Security Risks

Most AI money coach apps collect your financial data. Your responsibility is to review their privacy policies. Does the company sell anonymized data to researchers? Does it use your data to train its AI model? Does it share data with third parties?

Any platform that connects to your bank account is a potential target for hackers. Stash, MoneyCoach, and similar platforms use bank-level encryption and are SOC 2 certified, but no system is 100 percent secure. Your data is safer with them than on a spreadsheet, but there’s still some risk.

AI coaches aren’t licensed like financial advisors. If the advice causes financial harm, you have limited recourse. You can’t sue the AI coach. You might be able to sue the company, but the burden is on you to prove damages.

Behavioral Risks

Some people use AI coaches as a substitute for financial literacy. They follow the AI’s advice without understanding it. If the advice is wrong, they don’t catch it. This is dangerous.

AI’s tone is often authoritative (Transfer $500 to savings today). Users might believe that generic advice is personalized when it’s not. They trust the AI more than they should.

AI can nudge and remind, but it can’t provide emotional accountability. If you ignore the AI’s suggestions, there’s no consequence. A human coach would ask why you didn’t follow through. An AI just logs it and tries again tomorrow.

Practical Limitations

If you have money in multiple accounts (checking, savings, investments, crypto, foreign accounts), the AI might not see the full picture. It optimizes based on partial data. This leads to suboptimal recommendations.

If you get a promotion, lose a job, get married, have a child, or face health issues, the AI’s recommendations become outdated. You need to manually update your situation. Many people forget to do this.

AI can struggle with competing goals. You say “Save for a house down payment” and “Pay off student loans.” The AI might optimize for one and ignore the other. A human advisor would ask you to prioritize and create a strategy that balances both.

FAQ: Your Questions About AI Money Coaches and Human Advisors

Q: Can an AI money coach replace a financial advisor?

A: For simple situations (budgeting, basic debt payoff, beginner investing), yes. For complex situations (tax planning, estate planning, major life changes), no. AI is an assistant, not a replacement for human expertise. Think of it this way: an AI can handle routine financial decisions. A human advisor is needed when the stakes are high or the situation is unusual.

Q: How much can I realistically save by using an AI money coach instead of a human advisor?

A: A human advisor costs $150 to $300 per hour or 1 percent of your assets. An AI money coach costs $25 to $100 per month. If you use an advisor once per quarter (4 hours per year), you save roughly $600 to $1,200 per year by switching to AI. But AI can’t optimize investments or tax strategies the way an advisor can, so you might lose more in missed optimization. For example, tax-loss harvesting done right can save thousands annually. An AI coach won’t do that.

Q: Is it safe to share my financial data with an AI money coach app?

A: Most reputable apps (Stash, MoneyCoach, Sorted) use bank-level encryption and are SOC 2 certified. Your data is safer with them than stored on a spreadsheet. But review their privacy policy. Some apps sell anonymized data or use your data to train their AI. If privacy is a concern, use ChatGPT DIY instead (you control what you share).

Q: Which AI money coach is best for freelancers and side hustlers?

A: Sorted or ChatGPT DIY. Both handle irregular income well. Sorted has a feature for side hustle income tracking. ChatGPT can be customized specifically for your income pattern. Stash and MoneyCoach assume regular salary income, so they’re less suitable if your earnings vary month to month.

If you’re a side hustler exploring income opportunities, AI tools for affiliate marketing can help you identify revenue streams, though you’ll still need a money coach to manage the income properly.

Q: Can AI money coaches help me with investing?

A: Basic investing, yes. Robo-advisors use AI to manage a diversified portfolio automatically. But for complex investing (tax-loss harvesting, individual stock selection, alternative investments), a human advisor or specialized service is better. The difference is that AI manages your money according to pre-set rules. A human advisor can adjust for your unique situation.

Q: How long does it take for an AI money coach to become actually helpful?

A: Two to four weeks for budgeting advice (needs to see spending patterns). Two to three months for debt payoff strategies (needs to understand your income and obligations). Six months or more for investment recommendations (needs to understand your risk tolerance and time horizon). Early recommendations are generic. Over time, they become specific to your behavior.

Q: Can I use both an AI money coach and a human advisor together?

A: Yes. Many people use a human advisor for quarterly strategic planning and an AI coach for daily budgeting and accountability. This hybrid approach costs more but captures both expertise and real-time support. You get the planning from the human and the daily nudges from the AI.

Q: What should I look for when choosing an AI money coach?

A: Look at privacy policy (does it sell your data?). Check integration capabilities (does it connect to your bank?). Evaluate conversational ability (does it feel like coaching or just an app with suggestions?). Confirm use-case fit (does it handle debt payoff, investing, or budgeting?). Verify cost transparency (no hidden fees?). Read user reviews (does it actually help people?).

Mistakes to Avoid

You’re going to see people make these mistakes, and I want you to avoid them.

Mistake one: Treating AI recommendations as commands. An AI might say “Transfer $500 to savings today.” You do it because the AI said so, without thinking about whether you can actually afford it this week. AI gives advice based on patterns. If your pattern is unusual, the advice might be wrong. Always think critically.

Mistake two: Assuming an AI coach is personalized when it’s actually generic. The AI is personalized based on your data, but it can’t know everything about your situation. It doesn’t know about a job offer you’re considering or a major expense coming up next month. Don’t trust it with information you haven’t fed it.

Mistake three: Switching coaches too quickly. You try a coach for two weeks, see generic recommendations, and switch to another. AI coaches need 4 to 8 weeks to become useful. They’re learning about your patterns. Stick with one long enough for it to learn.

Mistake four: Expecting AI to handle complex situations it was never designed for. You’re going through a divorce and ask the AI for advice. It gives budgeting suggestions. You implement them, but they don’t address the core issue (splitting assets, tax implications, restructuring retirement accounts). This is a job for a human advisor, not an AI.

Understanding the broader AI landscape, including reading about how to make money with AI arbitrage, helps you think strategically about financial opportunities, but don’t mistake opportunity research for financial planning.

Mistake five: Giving up on your financial goals because an AI coach didn’t work for you. If the AI coach feels impersonal and you ignore its recommendations, that’s a signal that you need human accountability. Hire a coach. The tool doesn’t have to be AI. Sometimes human connection is what you need.

Key Takeaways

AI money coaches and human advisors serve different purposes. AI is best for budgeting, spending control, and behavioral nudges. Humans are best for complex situations, tax planning, and emotional accountability.

Cost matters. An AI coach costs $0 to $100 per month. A human advisor costs $150 to $300 per hour or 1 percent annually. The ROI of an advisor is high only if your situation is complex enough to justify the cost.

No single solution works for everyone. Choose based on your goals (budgeting, debt payoff, investing), budget, and comfort level.

For simple situations, AI is usually sufficient and more affordable. For complex situations, a human advisor is worth the cost.

Hybrid approaches are powerful. Use AI for daily support and human advisors for quarterly strategic planning.

Data privacy is a real concern. Review privacy policies before signing up. If privacy is critical, DIY ChatGPT is an option.

AI is not a magic solution. It’s a tool. You still need financial literacy and the discipline to implement recommendations.

Human advisors are not universally better. Many are excellent, but some are mediocre or have conflicts of interest. Do your due diligence.

Start cheap and simple. Use Sorted or ChatGPT DIY for 3 to 6 months. If you need more help, hire a human advisor. Don’t jump straight to expensive advice.

The best financial tool is the one you’ll actually use. If an AI coach feels impersonal and you ignore it, a human coach might be worth the money.

The tool matters less than your commitment. Whether you use AI or a human advisor, the results depend on you. You have to implement the recommendations and stick with the plan.

Your Next Step

Pick one goal: budgeting, debt payoff, or investing.

Try one solution for 30 days. AI option: Sorted ($0 free trial) or ChatGPT DIY ($0). Human option: one consultation with a CFP ($300 to $500).

Measure results. Did you save money? Did your habits improve? Did you feel supported?

Decide. If it works, expand. If not, try a different option.

Action beats perfect. Stop overthinking. Start today.

Disclaimer

This article is for educational purposes. It’s not financial advice. Consult a qualified financial advisor before making investment decisions. Especially for complex situations like tax planning, estate planning, or major life changes.

The income figures mentioned are illustrative. Past performance doesn’t guarantee future results. Individual results vary based on circumstances, discipline, and market conditions.

Leave a Reply